Memphis Rental Property #3

Last updated: 2026

NOTE: All figures and statements in this article were accurate as of the time of initial publication in 2024. I purchased this house in 2019. Check out the Annual Updates section at the bottom of the post to see how the property has performed since then.

Continuing on my journey to fill in the gaps in my Property Spotlights, let’s return to my third house and take a look at the deal.

I bought this house in May 2019, which was about six months after I had closed on Property #1. By this time, I had decided to go “all in” on cash-flowing rental properties and deploy all the cash from the sale of my primary NYC residence. This led to a flurry of acquisitions between May and September of 2019, by which time I had built the portfolio up to 16 properties.

In fact, “Property #3” is a bit of a misnomer. I closed on both Property #5 and Property #7 before this one, so technically it should be Property #5. Plus, I closed on four other properties on the same exact day as this one (!), meaning it could just as easily have been #6, #7, #8, or #9.

Nevertheless, this house is, and will forever be, Property #3. Why, you ask? Because that’s where I initially put it in my spreadsheet tracker, and it was just too much darn trouble to move it.

Anyway, the point is this: I was buying houses fast and furious in an effort to deploy my funds and build some cash flow. Property #3 through Property #16 were all purchased within about 120 days, so in a sense, we can think of them as a pack of 14 that were purchased (more or less) simultaneously.

With that context set, let’s get into the details of this investment property!

Property #3: The Deal

This house and Property #4 were purchased from the same seller, who had recently rehabbed both properties and placed new tenants. I liked that the properties looked nice and had new finishes, but the seller was not a turnkey operator I recognized. Were I buying these houses today, I would have asked a lot more questions, and been more sensitive to the risks associated with buying from an unknown flipper. I also would have paid more attention to the details of the rehabs themselves, since it turns out that the roofs had not been replaced, among other things. Therefore, they weren’t true turnkey rehabs, and I therefore should have thought about their value differently. (Live and learn!)

This was the first property I bought with a mortgage. I had realized that using mortgages was incredibly powerful for my long-term returns, so after purchasing Properties #1 and #2 with cash, I used mortgages on nearly all my acquisitions after that.

I bought this house off Roofstock. At the time, Roofstock was a new platform with some unique advantages: all exclusive listings that couldn’t be found elsewhere; helpful financial analysis tools built into the listing pages; due diligence already provided, including inspections and tenant ledgers; and the ability to make offers directly through the platform to the seller, without using an agent. Unfortunately, all of those aspects of Roofstock have since changed — it is now just an MLS listing aggregator trying to make money through agent referrals. As a result, I don’t recommend Roofstock to my private coaching clients anymore, as it doesn’t offer any incremental benefit to shopping for properties on Zillow.

Anyway, the house itself had 3 bedrooms and 1.5 baths, and was located in the Parkway Village neighborhood. This is a very solid C/C+ area, with most homes built in the 1950’s-1970’s, and it has become one of my favorite investment neighborhoods in Memphis. Here are some facts about this particular house:

Built in 1960

Central air

1275 square feet of interior space

Recent rehab with fresh paint & finishes

Hard-surface flooring except carpet in bedrooms

New tenant in place at $795

The property was offered at $79,000. My original offer was for $70,000. After several rounds of counter-offers, the seller agreed to a purchase price of $75,000. I signed the paperwork and we headed into the due diligence phase of the deal.

Property #3: Due Diligence

As mentioned, Roofstock provided an inspection document upfront, which looked very clean. The tenant had just been placed, so there was no payment history to review. However, I did know the tenant had been placed by a large, reputable PM, so I was confident that the screening standards used were reasonable.

Because I was using a mortgage, I also had an appraisal, which came in right at the purchase price of $75,000.

And that was pretty much it for due diligence! When you can see an inspection report before you make your offer, the due diligence phase becomes very easy. It was one of the really nice things about the old Roofstock before they made all those changes. (RIP, old Roofstock.)

I don’t have any good marketing photos for this property, but here are a few pics from the inspection report so you can get the idea:

Property #3: The Financials

I financed 67% of this purchase with a conventional loan at 4.93%, so my down payment was $25,000, and I incurred $2,721 in closing costs. I used the RIA Property Analyzer to run the final numbers on this property – here are the key metrics that the analyzer calculated for me:

Purchase Price: $75,000

Monthly Rent: $795

Monthly Cash Flow: $186

Cap Rate: 7.25%

Cash on Cash Returns: 8.09%

Total Returns w/ 2% Appreciation: 16.13%

(Want to use this calculator yourself? You can!)

OR

Using the multi-year model in the RIA Property Analyzer, we can visualize some of the main long-term trends, assuming an average inflation rate of 2%:

Cash flow increases over time. This is mostly because rent and expenses are expected to rise with inflation, but one major expense (my mortgage) is fixed.

Cash Flow Year 1: $2,242

Cash Flow Year 10: $3,302

Cash Flow Year 25: $5,549

Mortgage paydown accelerates over time. This is because of the way banks amortize loans – each month, a little bit more of your fixed payment is principal, and a little bit less is interest.

Mortgage Paydown Year 1: $748

Mortgage Paydown Year 10: $1,164

Mortgage Paydown Year 25: $2,432

Total returns on cash increases over time. This is a consequence of the first two graphs – I will make greater total returns over time on the same initial investment of cash.

Total Returns on Cash Year 1: 16.20%

Total Returns on Cash Year 10: 22.58%

Total Returns on Cash Year 25: 37.49%

Overall, this was a very solid cash flow property. I was able to achieve 8%+ cash-on-cash returns, which I consider very good. I think I got a reasonable deal on the house, and I really like the neighborhood. In hindsight, though, if I could go back and do anything differently, I would have paid more attention to the condition of the major cost centers such as the roof and HVAC. (If you continue down through the Annual Updates, you’ll see that this came back to bite me a bit.)

Property #3: The Deal Sheet

Finally, to sum up Property #3 and its financials, here’s the full “deal sheet”:

Looking for YOUR Next Property?

If you need help finding, analyzing, and purchasing YOUR next property — or your first one! — schedule a free initial consultation with me. I’ve helped dozens of private coaching clients invest with confidence and build cash-flowing rental portfolios of their own.

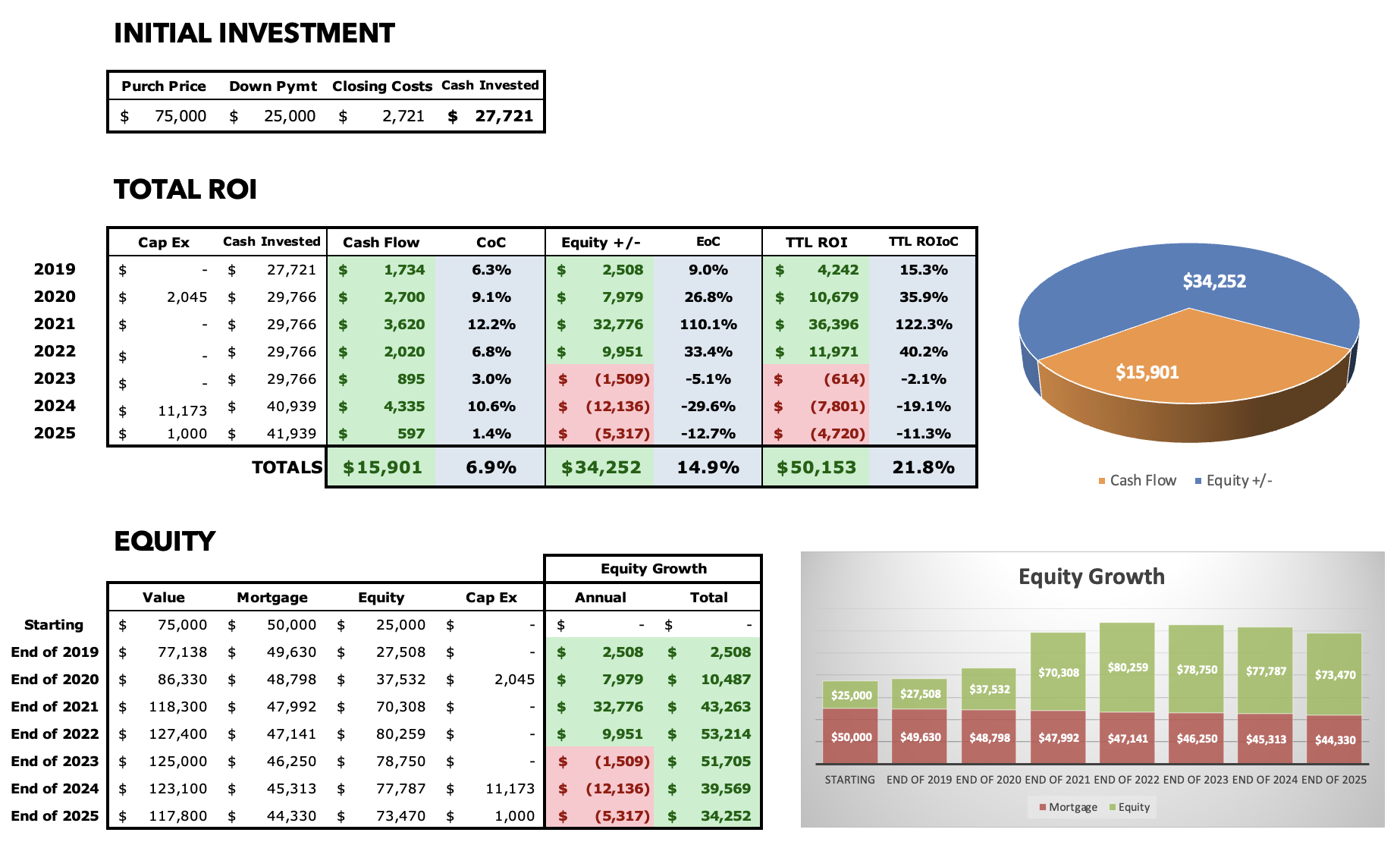

Annual Updates

For all Property Spotlights, I come back at the end of each year to provide a brief narrative of what happened at the property that year. I also update my annual and cumulative figures for the property, including cash flow, equity growth, and occupancy.

2019

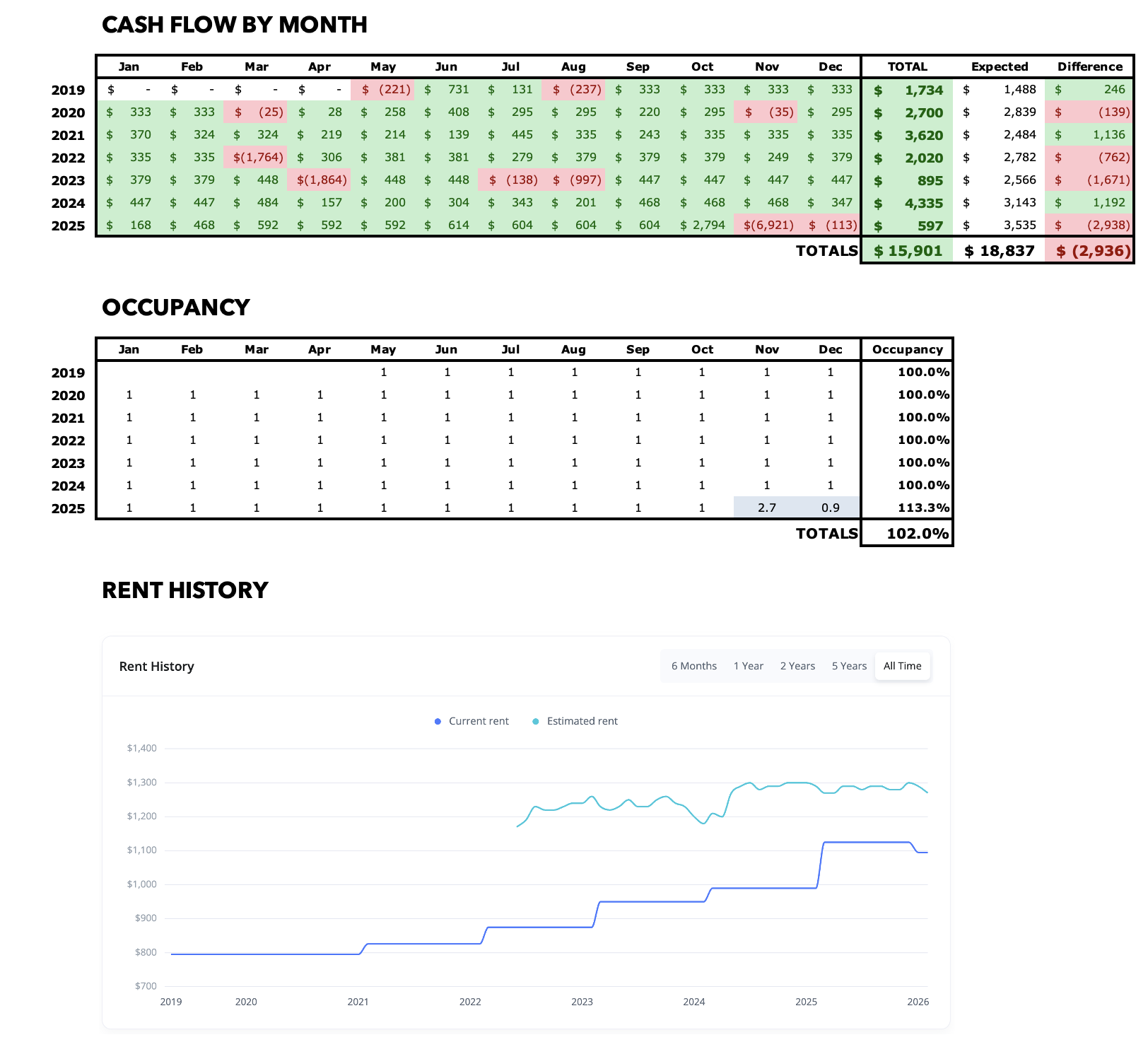

Because the property was occupied, I was able to cash flow from Day 1. The one significant expense was to repair a roof leak, which was the first of numerous recurring issues with the roof. Still, the house produced a few thousand in cash flow, exceeding my target.

2020

There were several small maintenance issues, including another small roof repair and several HVAC repairs. I was eventually forced to replace the HVAC condenser, incurring a $2K capex charge — but officially my cash flow doesn’t include CapEx, so I still showed a $2,700 profit for the year which was very close to my target.

2021

The tenant renewed their lease at the beginning of the year, with an increase to $826/mo. Not much else to report — low maintenance costs allowed me to exceed my cash flow target by over $1K. Like all my properties, appreciation was very strong this year as well.

2022

The tenant renewed their lease once again, this time at $875/mo. Even with these annual increases, we’re not keeping up with market rents, which are rising much faster. So we’ll need to keep raising rents each year, though the tenant occasionally pays the rent late, so I don’t want to push too hard. The property produced $2K in cash flow this year, but that fell short of my target due to a large maintenance expense — once again, it was the roof, and the repair cost me $2,145.

2023

The tenant signed on for another year, with an increase to $950/mo. Still very much below market rent, but closer — and at least I’m avoiding the turn. In fact, this is one of only a handful of my properties that still has the original tenant in place from the time of my purchase.

Unfortunately, maintenance expenses were very high this year. This reduced my cash flow for the year to just $895, significantly below my target. The tree in the front yard had to be removed at a cost of $2K+, and I also had a few plumbing calls and (you guessed it) another roof repair costing almost $1K. Home prices have leveled off — in fact, my annual equity growth was slightly negative on this property.

2024

The tenant renewed once again, with a new rent of $990/mo. While this is still quite a bit below market rent, I’m happy to continue with incremental increases for this long-term tenant.

While total maintenance costs were reasonable ($1,300), but on the CapEx side my repeated roof repairs finally gave way to a full roof replacement — which in hindsight perhaps I should have done from the outset. That cost me $8K, and I invested another $3K in new LVP flooring after the existing flooring was damaged by a large leak caused by a backup in the HVAC condensate line. So while cash flow was technically strong this year at over $4K, I had to put ~$11K back into the house.

2025

With the tenant significantly below market rent, we went for a larger increase to $1,125/mo. on their renewal. Unfortunately, the tenant had to break their lease early for personal reasons. To their credit, they were open and communicative about this with my PM. They agreed to pay the lease-break fee (two month’s rent), and lost their security deposit as well, but on account of this I waived all the moveout charges that would otherwise have been charged to them. This extra revenue also explains why my occupancy exceeded 100% for the year.

This was the first time I had ever turned this property, so there was quite a bit of work to do — the turn cost over $7K, plus another $1K in CapEx (replacement of the bathroom vanity and sink). Despite this, I was able to eke out a small amount of positive cash flow for the year.

Fortunately, a new tenant moved in just 34 days after the previous tenant vacated, paying $1,095/mo. on a two-year lease.

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.