What the Chaos in the Home Insurance Industry Means for Rental Property Investors

The normally staid home insurance industry has been in the news quite a bit recently. Due to the increasing costs of paying out claims in some areas, insurers are making unprecedented changes: rapidly increasing premiums, halting the issuance of new policies, and in some cases canceling policies and pulling out of entire states altogether.

This is consequential for people who own their primary residence, of course. But it’s also very important for those of use who invest in rental properties. We need insurance, too, and this industry shake-up should change the way we think about our investments.

In this article, I’ll review what’s happening with home insurance, why it’s happening, and where the impacts are most severe. Then I’ll share some important takeaways and strategies for rental property investors — what you should know, what you should do differently, and what it means for where and how you invest.

What’s going on with home insurance?

The answer here is pretty simple: home insurers are losing money.

This might be a hard truth to swallow if you’ve ever fought with an insurance company over a claim. The nature of the insurance business is that customers pay regularly for a long period of time, receiving no benefit, and then when they finally need to use their insurance, their provider will be stingy and reluctant to pay. Nobody loves their insurance company, and they are easy villains.

Can these miserly jerks really be losing money? Well, yes. In fact, home insurance as a business was unprofitable in 18 states last year, and the problem has been getting gradually worse in the last decade. This great analysis shows the historical profitably of insurance by state — check it out to see what’s happening in your state. Here’s a sampling of them — green is profit, red is loss:

Source: New York Times

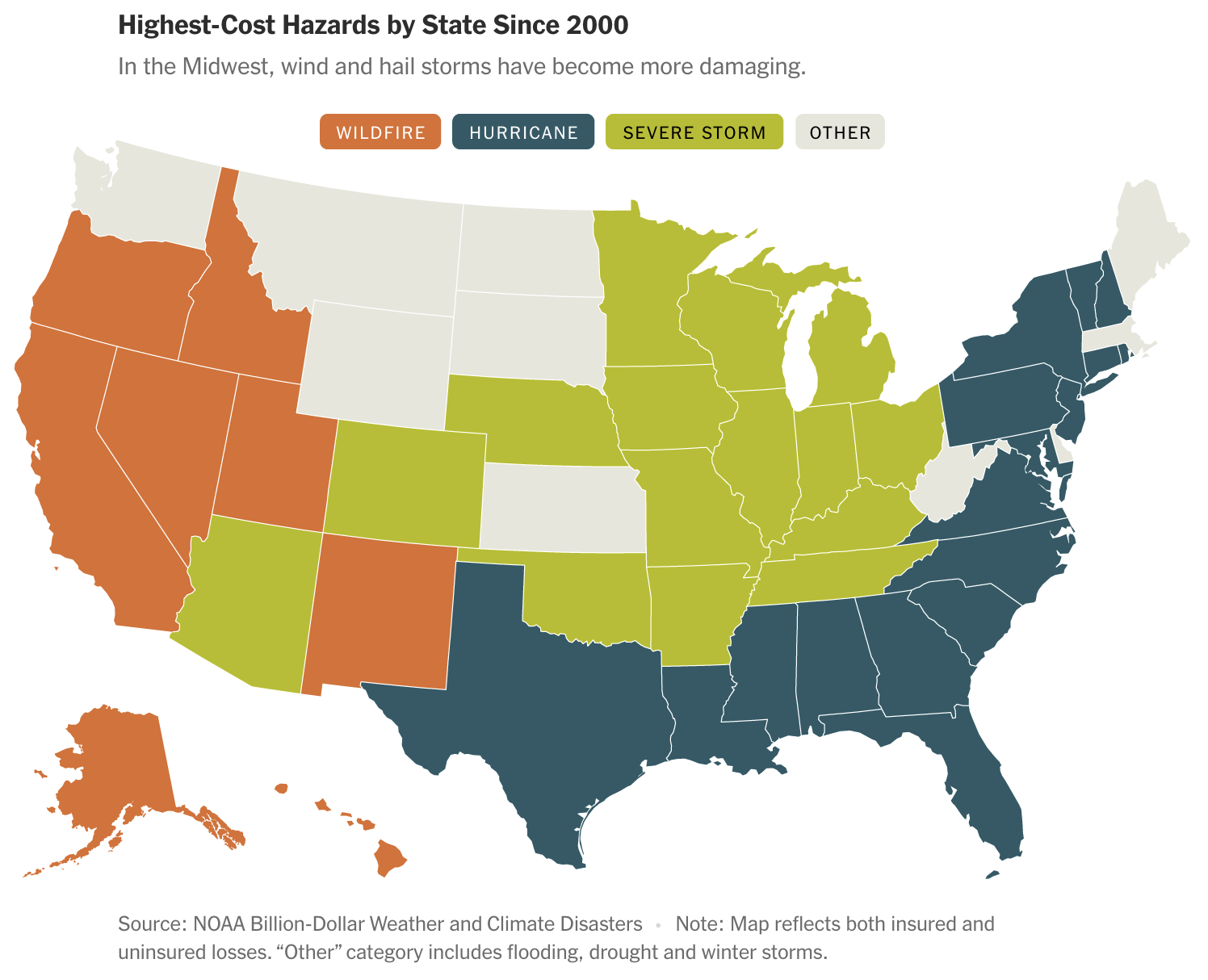

What’s driving down home insurance profitability? The cost of claims has risen rapidly, driven mostly by hurricanes, windstorms and hail, and wildfires. All of these events are exacerbated by climate change, and by the expansion of housing development in high-risk areas. This eye-opening piece on sunny day flooding in coast North Carolina paints a clear picture of the inexorable rise of these threats. (To be clear, home insurance does not cover flood damage; nonetheless, the point is that these and other climate-fueled threats are growing, and will continue to do so in the years to come.)

Insurers are businesses, and like all businesses they seek profit. So they have responded to these losses by raising premiums (by double-digits in 2023) and limiting their exposure in certain places by canceling policies or pulling out of states altogether. This has left many homeowners with few options, and caused state governments to scramble in an effort to stabilize their insurance markets and lure back insurers who have backed away. (And if you think you’re protected from these shifts if you live in a condo, think again: condo associations are also facing huge increases in their insurance costs, which will be passed on to condo owners in the form of monthly HOA fees.)

I’ve experienced this personally. We own a condo in Florida that we use during the winter. Because condo policies don’t insure the structure itself (which is covered as part of the full condominium’s insurance), they tend to be relatively cheap. When I first got my policy from Allstate a few years ago, it cost about $950. But when I went to renew last fall, I was told that my insurance company was leaving the state of Florida, and there was no other insurer who would write a new policy for me. That left me with only one option: Citizens Insurance, which is the entity backed by the state of Florida and considered the insurer of last resort. (Many other states have similar “last resort” programs that are now playing a more prominent role as private insurers retreat.) My new policy cost me $1,800, nearly double what I was paying before. And I’m not alone in having to move my coverage to Citizens: so many other Floridians have done so that Citizens is now the state’s single largest insurer.

But isn’t this just a local problem in high-risk areas? Actually no — the effects are being felt all over the country. Plus, home insurance plays a larger role in the economy than you might realize, and there are potential broader risks in play here.

Why home insurance is an economic necessity

The pooling of risk that results from near-universal home insurance is not just important for individual homeowners, who might face economic calamity if their home — likely their largest asset — were to be destroyed or damaged. It’s also important for lenders, and therefore for the broader housing market.

If a buyer can’t get insurance on a property, they also can’t get a loan, because lenders will require insurance to be sure that their loan is repaid if a catastrophic loss occurs. Without loans, many people couldn’t buy their homes, which could reduce overall demand and put downward pressure on home prices.

The same thing could occur even if insurance was available, but became much more expensive than it used to be. If it costs, say, $12,000 per year to insure a home rather than $4,000, fewer people can afford that home, and its value will go down.

Further, if state-backed insurance pools become much larger, state budgets and tax rates could be impacted. For example, elected officials in Florida have sounded warnings about another significant storm like Hurricane Ian in 2022, saying that the state might not have sufficient funds to cover a large disaster now that so many people are part of the state insurance plan. States are required by law to balance their budgets — so if the state has to pay out billions in claims, that money must eventually come from taxpayers.

What does this mean for rental property investors?

The reckoning in the home insurance industry is of significant concern to rental property investors. Having proper coverage is important to reduce your risk, of course. But higher insurance costs will also eat into cash flow, which is one of the major draws of owning rental properties.

Here are some ideas and strategies to help mitigate the impact to your rental property investing:

Reduce your property coverage

The main driver of your insurance premium is the amount of property coverage you carry — in other words, how maximum amount the insurance company will pay in the event of a total loss. Policies are often written to cover “full replacement value”, an amount that can be much more than you paid for the house, and more than it’s currently worth. If that’s the case, you may be comfortable reducing your property coverage such that it only covers your investment in the property. In doing so, you’d still be made whole in the event of a total loss of the property, but save a bit on your premium. (Note that you may be subject to a minimum property coverage per square foot, which will create a “floor” of property coverage that you can’t go below.)

You can also look to eliminate other optional coverages (such as Loss of Rents insurance) from your policies to reduce your costs.

Look for a large group plan

You can benefit from being part of a group insurance plan, in which many owners pool together to negotiate their policies with an insurance provider. In my case, I’m able to access group plans through my property manager, who has an arrangement with a local insurance company. These plans have competitive rates, and may reduce your exposure to large annual increases in your premiums due to the stronger negotiating power of the group.

Buy homes in safer areas

The best-case scenario is to HAVE insurance, but never have to USE it. When considering which markets to invest in, climate and weather risk should be a big part of your thought process. You may want to:

avoid coastal markets with tropical storm risk

avoid markets with severe winters

avoid markets (and individual properties) with wildfire risk

Also, a word about flood risk. While flood damage is not covered by regular homeowners insurance, it’s still important to avoid flood risk, which is primarily a consideration at the level of an individual property (rather than a total market). I use RiskFactor to assess the flood risk of any properties I’m evaluating for myself, or for my private coaching clients. RiskFactor has also recently added models for wildfire risk and wind risk.

Buying in safer areas not only makes it less likely that you’ll have to use your insurance — it also means your insurance will probably be cheaper, and makes it less likely that you’ll face eye-popping annual increases in your premiums. In the end, your insurance costs will correlate with the underlying risk: the higher the risk, the more expensive it will be to insure.

Self-insure

Dropping your insurance coverage altogether exposes you to significant risk, of course. Still, it may be a reasonable choice for investors with large portfolios who are able to absorb a total loss at a single property, such as a house fire. With a large portfolio, the annual savings from self-insuring may justify the additional risk.

However, this is an “end stage” strategy for large investors, and won’t be right for most people. It’s particularly risky if your portfolio is in an area that could face damage over a large geographic area and impact multiple houses, such as from a hurricane or wildfire. Also, this is only an option for properties that you own without a mortgage — if you have a loan, your lender will require that you carry insurance.

Conclusion

Home insurance is facing a reckoning as the cost of claims increases and insurers struggle to remain profitable. This has broader implications for the housing market, and for rental property investors.

In addition to planning for higher insurance costs, investors should consider other mitigation strategies, including:

reviewing their existing policies to see if reducing coverage is appropriate

looking for a large group plan

buying in safer areas and assessing risk more accurately with tools like RiskFactor

self-insuring (large investors only)

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.